Electronic payments is one of the fastest growing areas in fintech. Since we have a number of electronic payments companies in our Spaceship Universe Portfolio, it’s worthwhile to delve into this interesting and constantly evolving space.

The value chain

Electronic payments seem simple. Let’s say you’re buying your morning coffee. You take out your phone, with Apple Pay installed and linked to a debit card, and tap it against the terminal. ‘Accepted’ (hopefully) flashes on the terminal and you walk away with your coffee, knowing your bank account has been charged $3.50.

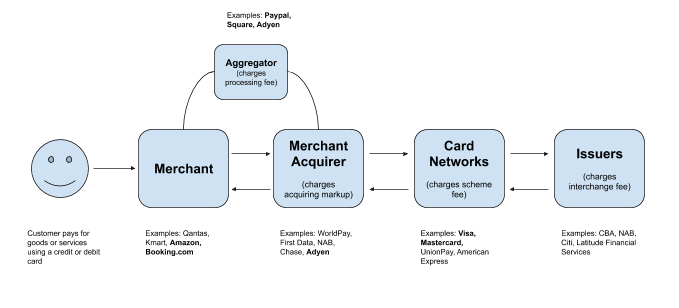

However, in reality, the transaction data from your coffee purchase passes through a complicated chain of different entities. We’ve drawn a simplified flow chart below that maps the main entities.

As the merchant, the coffee shop will typically use a payment terminal to process the debit card payment (through the Apple Pay mobile wallet) using near-field communication (NFC) technology.

The payment terminal sends the transaction information to a merchant acquirer that it has an agreement with. Merchant acquirers provide merchants with access to the card networks. The merchant acquirer usually also performs some risk management checks. They are financially exposed to merchant defaults and merchant fraud, as they are typically responsible for chargebacks from goods and services not delivered. Traditional merchant acquirers for point-of-sale transactions include the big banks like CBA and NAB and large global merchant acquirers such as WorldPay and First Data.

The merchant acquirer then passes the transaction to the card network, typically Visa and Mastercard. Card networks connect and switch transactions between merchant acquirers and issuers, enabling payment authorisation. They are also responsible for clearing and settlement of the transaction.

The card network identifies the issuer of the debit card, which is typically your main bank. The issuer will validate your identity and provide authorisation to the card network. Issuers are financially exposed to fraud, such as the unauthorised use of your debit or credit card.

The card network forwards the authorisation back to the merchant acquirer and then the transaction is authorised on the transaction terminal, allowing the coffee shop to know that the payment has gone through.

Over time, additional participants have joined the value chain. A good example are the aggregators, which include Paypal and Square, which allow sellers to accept payments without setting up a cumbersome merchant account with a traditional merchant acquirer.

Layers of fees

As you can imagine, all these intermediaries charge their own fee, usually both as a percentage of the transaction value and/or a relatively small flat fee. The fees are typically passed on through the chain to the merchant and embedded into the price of the good or service being sold/provided. Some merchants choose to pass along the cost to the shopper, as an extra fee to the shopper upon payment using an electronic payment method.

The issuer of the debit or credit card has traditionally charged the largest part of the total fee. This is called the interchange fee and according to Adyen can vary significantly based on country and region, card brand, whether it’s debit or credit and the size of the merchant. In the US, the average interchange fee is around 2% and can go up to around 3.50%. In the EU, interchange fees are much lower, since the government caps it to 0.3% for credit cards and 0.2% for debit cards. In Australia, interchange fees were capped by the RBA recently, at 0.88% for credit cards and 0.22% for debit cards.

The card networks, merchant acquirers, payment processors and payment aggregators all charge their own additional fees.

How are fintech players innovating in the space?

As e-commerce transactions have boomed, mobile and web payment gateways such as Stripe, Paypal and Adyen have become just as important as point-of-sale terminals. Adyen is also a merchant acquirer in its own right.

Digital wallet services, such as Paypal, Venmo and Apple Pay, continue to grow in popularity. Paypal-owned Venmo counts more than 40 million active accounts, more than some of the largest US banks. Only JP Morgan reported more digital users in the same time period. Contactless payment and mobile payment is becoming ubiquitous, particularly in Australia where NFC enabled point-of-sale terminals are the norm.

Why are Visa and Mastercard so hard to disrupt?

Banking is a fragmented market globally, with more than 25,000 banks in the world. However, nearly all banks issue Visa or Mastercard branded debit and credit cards. Visa was founded in 1958 and Mastercard in 1966. The other major card networks include American Express (who specialise in the prestige segment of the market) and UnionPay in China. China has not yet allowed Visa and MasterCard to enter its domestic payments scene.

We consider that up and coming payments platforms such as Adyen, Stripe, Paypal and Square, have the potential to disrupt Visa and Mastercard, given their popularity and global scale. But so far they have chosen to work with Visa and Mastercard, and facilitate payments made with Visa and Mastercard credit and debit cards, in order to more quickly build their user base and scale. Paypal-owned Venmo actually issues its own Mastercard-branded debit card.

Emerging economies are different

The bigger threat to Visa and Mastercard’s dominance over the long term could be whether it can bring its business model to emerging markets, where some 2 billion people do not have a bank account and still transact mostly in cash.

A trend that has been playing out in emerging economies is the adoption of mobile payment systems that often bypass credit and debit cards (and therefore Visa and Mastercard). For instance, mobile payment system M-Pesa has become dominant in its home market Kenya, and other emerging economies. M-Pesa transactions now amount to nearly half of Kenya’s GDP. According to the BBC, high penetration of mobile phones allowed users to leapfrog its inefficient and inadequate banking system, which didn’t serve the low income majority.

WeChat Pay (owned by Tencent) and Alipay (owned by Alibaba) have become ubiquitous in China for their simplicity and convenience. Most users of WeChat Pay transfer money from their bank account to their WeChat Pay wallet, again bypassing card networks.

While banks and credit and debit cards dominate in the US, there are signs of new things to come. For instance, Square’s Cash app in the US recently started supporting direct deposits, meaning users can get their paycheck directly into their Cash app balance. This allows them to serve underbanked communities, and puts Square one step closer to replacing banks.

Bottom line

Given the large fees currently charged to merchants in many parts of the developing world, it’s fair to say that banks and card payment networks are vulnerable to changes in regulation and technology firms, especially if they attempt to capture more of the value chain.

In emerging economies, technology firms have already become dominant, providing a better service to both merchants and customers, and taking a smaller cut of the transaction. In the Spaceship Universe Portfolio, we’re invested in some of the key technology companies that benefit from these dynamics, such as Tencent, Square, Paypal and Adyen.

“This is going to be the battle of all time—like who dominates all those services—and it’s still not known,” Jamie Dimon, CEO of JP Morgan, told investors in early 2018. “Everyone wants to be the place that is the one place you go to do that.”

The Spaceship Universe Portfolio currently invests in Alibaba, Tencent, Paypal, Square, Adyen, Visa and Mastercard.

The Spaceship Index Portfolio currently invests in Alibaba, Tencent, Paypal, Visa and Mastercard.

Important! We’re sharing with you our thoughts on the companies in which Spaceship Voyager invests for your informational purposes only. We think it’s important (and interesting!) to let you know what’s happening with Spaceship Voyager’s investments. However, we are not making recommendations to buy or sell holdings in a specific company. Past performance isn’t a reliable indicator or guarantee of future performance.