We pay our taxes, we vote and, as a part of this social contract, the government makes and enforces laws and regulates aspects of human society. Armed with our tax dollars and a mandate given by the people, they are supposed to act in our best interests. However, the more abstract areas of society the government moves into, the blurrier the lines get around the role of the government and what their role really is.

Take superannuation for example, the government has mandated that we pay 9.5% of our salary into a superannuation fund. Regulatory bodies such as APRA and ASIC are carefully watching over the industry. The mechanism used by superannuation is a trust, placing fiduciary duties on the trustees to act in the best interest of the members of the fund. There are plenty of checks and balances throughout the process to minimise the risk of malfeasance, and to ensure your money is safe. So, we can’t blame you from thinking that your Super is (for want of a better word) ‘safe’. However, at the crux of superannuation is investment, and more importantly return on investment, or else the super guarantee would just be put in a bank account. Whenever money is being invested with potential returns there is always a level of risk.

So within super we have the yin and yang of risk and return…

RISK: *The chance the amount earned (the returns) on your investments is different (higher or lower) than what you expect.*

RETURN: *How much you earn on your investment*

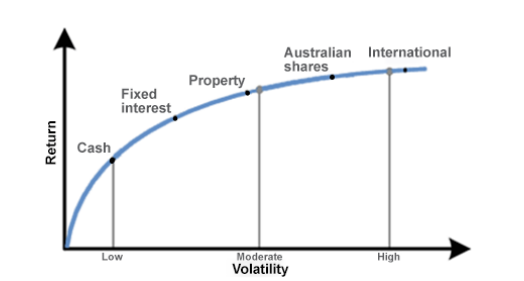

Investing always carries some degree of risk and the level of risk will depend on the nature of the underlying investments and the approach taken to achieve a return. As you can see from the diagram below, international shares contain the highest level of volatility, which is a form of risk, but they can also provide the highest return. The idea is that investors expect a higher return for taking on additional risk, otherwise they wouldn’t take on the additional risk.

However, before we contemplate our risk appetite and think about how prepared we are for fluctuations in investment returns and account balance, one of the biggest risks you face is not having enough to support your retirement expectations. So, before you consider what sort of investment option you want to be in, one of the first questions you should ask yourself is, “how much will I need when I retire?”

Once you have considered how much you need, or what sort of expectations you have around your retirement savings, it’s then worth thinking about your risk profile. Based on your risk profile you will have different expectations on returns and how long you want to stay invested for. This risk profile may vary over times, as you get older and your circumstances change. It’s always important to factor in what sort of investment objective you have, whilst being cognisant of your risk appetite.

There are generally considered 5 different risk profiles:

Cautious:

- May be unwilling to accept a short-term loss

- Short-term investment horizon (less than 1 year)

- May choose to invest in 100% defensive assets

Defensive:

- Priority is the preservation of capital in the short-term (little tolerance for loss)

- Short-term investment horizon of 1–3 years

- Majority of portfolio in defensive assets 65–85% with a small allocation to growth assets

Moderate

- Some exposure to growth assets to increase returns over a short to medium-term period.

- Have some tolerance to year-to-year variation, including an occasional negative return

- Minimum investment timeframe of 2–5 years

- May choose to invest 40–50% in growth assets

Assertive

- Substantial exposure to growth assets to increase returns over medium to long-term

- Accept short-term fluctuations in value investments, including negative returns, with an aim for higher returns over the long-term

- Minimum investment horizon of 5–7 years

- May choose to invest 60–80% in growth assets

Aggressive

- High exposure to growth assets to increase the likelihood of a greater investment return over the long-term

- Strong tolerance for short-term fluctuations in the value of investments, including negative returns with an aim of maximising returns over the long-term

- Typically has a minimum investment horizon of 7–10 years

- May choose to investment over 80% in growth assets

Understanding your risk profile and expectations around your retirement savings are important in helping you understand what investment option and super fund is for you.